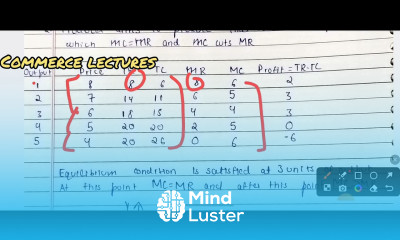

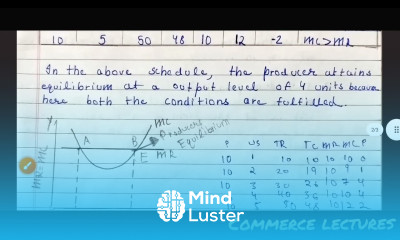

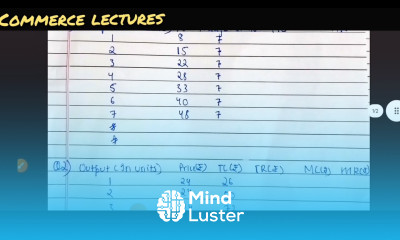

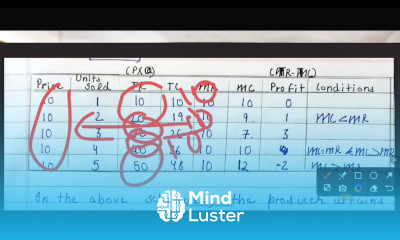

producer equilibrium,

in this course gain a deep understanding of how producers make optimal decisions to maximize profit. In this course, we will learn about the concept of producer equilibrium, where a firm reaches a level of output at which it has no incentive to increase or decrease production because it is earning the highest possible profit. You will explore different approaches to analyzing producer equilibrium, such as the marginal cost and marginal revenue (MC = MR) method and the isoquant-isocost approach. The course will explain both short-run and long-run equilibrium conditions, the role of cost structures, and how market types affect producer decisions. With diagrams, real-life examples, and practical exercises, this course helps you understand the logic behind production decisions and profit maximization. Ideal for economics students and business learners, this course builds a solid foundation for understanding firm behavior in various market structures. Join now and master the principles of producer equilibrium. Commerce lectures