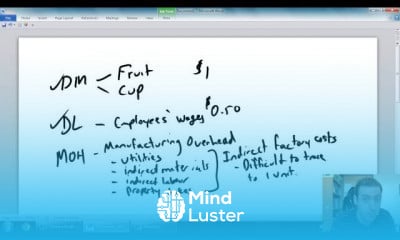

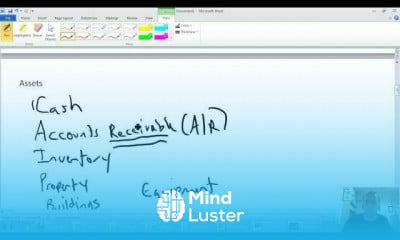

Quality of Earnings Analysis | Working Capital

Share your inquiries now with community members

Click Here

Sign up Now

Lessons List | 5

Lesson

Comments

Our New Certified Courses Will Reach You in Our Telegram Channel

Join Our Telegram Channels to Get Best Free Courses

Join Now

We Appreciate Your Feedback

17 Reviews

Dr.Ghvs Sarma

Isra mohamed mohumed

Akash Umbadwad

Andi Yusman

Show More Reviews

Related Courses in Business

Course Description

How do you measure quality of earnings?

The quality of earnings ratio, sometimes referred to as the quality of income ratio, is calculated by dividing the net cash provided by operating activities by the net income of the business.What is a good quality of earnings ratio?

A ratio of greater than 1.0 indicates a company has high-quality earnings, and a ratio of less than 1.0 indicates a company has low-quality earnings. Earnings quality refers to the amount of earnings that come from the business operations themselves, like sales and operating expenses.What is the point of a quality of earnings?

Why a Quality of Earnings Report? A quality of earnings report helps to establish the value of a business by analyzing and reporting on detailed aspects that may not be readily identifiable to a seller, buyer or investor in reviewing the financial statements.Why do users assess earnings quality?

Evaluating the quality of earnings will help the financial statement user make judgments about the “certainty” of current income and the prospects for the future.Who prepares a quality of earnings report?

A quality of earnings report provides a detailed analysis of all the components of a company's revenue and expenses. These reports are frequently prepared by independent third party firms during due diligence in an acquisition.

Trends

French

Graphic design tools for beginners

Data Science and Data Preparation

Formation efficace à l écoute de l

Artificial intelligence essentials

Learning English Speaking

Essential english phrasal verbs

MS Excel

American english speaking practice

Electrical engineering for engineer

Build a profitable trading

Build a tic tac Toe app in Xcode

Python for beginners

Figma for UX UI design

YouTube channel setup

Magento Formation Français

Web Design for Beginners

Computer science careers

Marketing basics for beginners

ArrayLists in C for beginners

Recent

Data Science and Data Preparation

Growing ginger at home

Gardening basics

Ancient watering techniques

Grow mushrooms

Growing onions

Veggie growing

Bean growing at home

Growing radishes

Tomato growing at home

Shallot growing

Growing kale in plastic bottles

Recycling plastic barrel

Recycling plastic bottles

Grow portulaca grandiflora flower

Growing vegetables

Growing lemon tree

Eggplant eggplants at home

zucchini farming

watermelon farming in pallets