Course Description

What are support department costs?

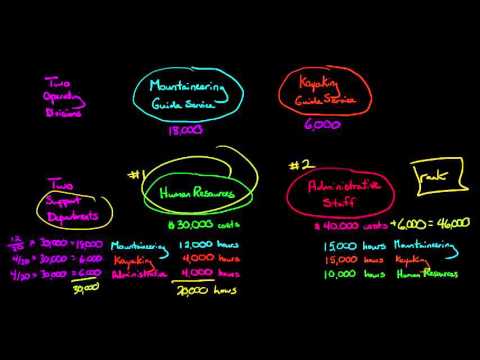

Allocate support department costs to producing departments. The support department costs are part of the total product costs and must be assigned to the products through cost allocation from support departments to producing departments. 4. Calculate predetermined overhead rates for producing departments.How do you allocate support department costs?

There are three methods of allocating support department costs: the direct, step-down and reciprocal. The key differences among the methods are the assumptions as to how services provided by one support department are allocated to other support departments.What are support departments and why are there costs allocated to other departments?

The costs of service departments are allocated to the operating departments because they exist to support the operating departments. Examples of service departments are maintenance, administration, cafeterias, laundries, and receiving.