Course Description

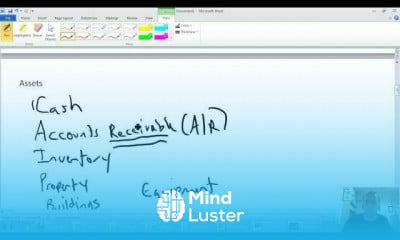

An intangible asset is an asset that is not physical in nature. Goodwill, brand recognition and intellectual property, such as patents, trademarks, and copyrights, are all intangible assets. Intangible assets exist in opposition to tangible assets, which include land, vehicles, equipment, and inventory.What are intangible assets on balance sheet?

An intangible asset is a non-physical asset that has a multi-period useful life. Examples of intangible assets are patents, copyrights, customer lists, literary works, trademarks, and broadcast rights. The balance sheet aggregates all of a company's assets, liabilities, and shareholders' equity.How do you identify intangible assets?

Intangible assets are measured initially at cost. After initial recognition, an entity usually measures an intangible asset at cost less accumulated amortisation. It may choose to measure the asset at fair value in rare cases when fair value can be determined by reference to an active market.